Although Kashirah Jackson is back at work, she’s still far from recovering from the economic upheaval the coronavirus pandemic wreaked on her finances.

Early last year, the independent hair stylist’s business in Charlotte, North Carolina, was doing well and socking away her earnings for a down payment on a home. But the state lockdown left her unable to see her clients and forced her to deplete her savings so she and her 1-year-old daughter could survive.

Now, only about 60% of her customers have returned. And though Jackson is still collecting some unemployment benefits, her income remains down from pre-pandemic times.

What’s worse, the spike in housing values over the past year will make it even tougher for her to buy a place of her own any time soon.

“Now, I will have to work harder and longer to get back to where I was,” said Jackson, 35, adding that as a renter, she can’t refinance a mortgage like those who own homes can to help cover their expenses. “My only cushion was my savings.”

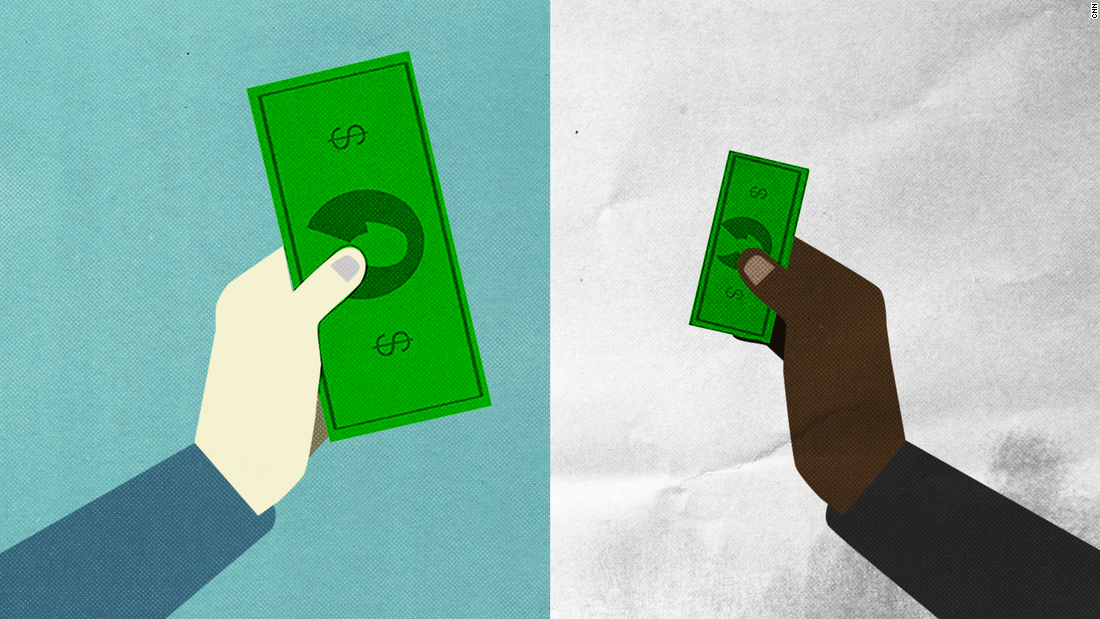

While the coronavirus pandemic has cut a wide swath through many people’s bank accounts, it has also highlighted the economic insecurity that many Black Americans face.

A quarter of Black Americans said their current financial situation was worse now than it was a year ago, before the pandemic, compared to 17% of their White peers, according to a Pew Research Center survey conducted earlier this year. Among adults who are usually able to save, 44% of Black respondents said they are saving less than they were in early 2020, compared to just over a quarter of White Americans.

And far more Black Americans reported being concerned about being able to afford food, cover their rent or mortgage and pay their bills, said Khadijah Edwards, a research associate at Pew.

This inequity stems in part from Black Americans having far less wealth and savings to turn to during tough times than White Americans. And the gaps also give Black households less of a springboard to recover when the economy picks up again.

“If you don’t have the wealth, it’s a gamble of how you are going to be on the other end,” Fenaba Addo, associate professor of public policy at the University of North Carolina at Chapel Hill, said of the pandemic-fueled downturn’s impact on Black Americans. “It may be a while before people are able to rebuild themselves and their families from this.”

The typical non-Hispanic White household had a net worth of $188,200 in 2019, compared with $24,100 for a non-Hispanic Black family, according to Federal Reserve Bank data.

The big difference in homeownership, which is key to building wealth, accounts for part of the chasm. It’s often more difficult for Black Americans to buy homes because they have lower median incomes, are less likely to receive inheritances or assistance from their parents and must contend with historical racism in real estate and its lasting impacts.

Only 45% of Black Americans own homes, compared to nearly 74% of White Americans, according to the most recent Census Bureau data.

Also contributing to their vulnerability: Black Americans are much less likely to invest in stocks or mutual funds than White Americans and have less than a quarter of the savings set aside for emergencies.

The lower rates of homeownership and investing mean that many Black Americans are missing out on the robust gains in the housing and stock markets over the past year that have greatly benefited others.

Homeowners with mortgages gained an average of $33,400 in home equity between the first quarters of 2020 and 2021, according to CoreLogic, which analyzes property data. And the stock market is at or near record highs.

If Harold Jones owned a home or had more than a few hundred dollars in investments, he says he would not have had to upend his life to make it through the pandemic after losing his job with a wildlife control company in March 2020.

Though he received enhanced federal unemployment benefits and cashed in his tiny retirement account, he still had to downsize to a smaller apartment in Baltimore, Maryland, and give up his beloved 2008 Subaru Impreza, which he used to visit his mother, see friends and go to the beach and on hikes.

Jones now has a better, albeit contract job with the Baltimore school system as a student support aide that he hopes will turn into a teaching position, as well as a part-time gig as a bartender. Still, the pandemic has set back both his career and his wallet.

“Coming out of the pandemic without a nest egg or something you can liquidate puts you at a disadvantage,” said Jones, 34, adding that he could have been better prepared for the downturn had he learned about finances and savings when he was younger. “I would have gladly sold some stock to get $1,200 to fix my car.”

Like Jones and Jackson, many Black millennials are in a particularly tough spot. Even prior to the outbreak, the generation overall had accumulated less wealth than Baby Boomers and Gen Xers did at the same age. That’s in part because they came of age at the worst possible moment — when the economy collapsed after the 2008 financial crisis.

Despite the prosperous economic times that existed between 2016 and 2019, older non-Hispanic Black millennials fell even further behind expectations set by prior generations at the same age, according to the Institute for Economic Equity at the Federal Reserve Bank of St. Louis. Their median net worth of $5,000 was 52% lower than expected in 2019. Three years earlier, their median wealth was 39% lower.

Older non-Hispanic White millennials, meanwhile, narrowed the gap in their expected wealth over those three years, according to the institute. The typical family had a net worth of roughly $88,000 in 2019, only 5% below expectations, compared to a shortfall of 40% in 2016.

Millennials impacted by student debt crisis

One thing that is weighing down older Black millennials, who were born in the 1980s, is student debt. Some 81% of college graduates in this group have student loans, with a median value of $52,000, compared to just over half of older White millennials, whose median balance is $40,000, according to Federal Reserve Bank data.

To give Americans a fiscal hand during the pandemic, Congress and the Trump administration suspended the repayment of federal student loans. President Joe Biden extended the pause through September. This aid, along with more generous unemployment benefits, three rounds of stimulus payments and a moratorium on evictions, has helped keep people afloat during the outbreak.

But most of these programs will run out in the coming weeks and months — which concerns some experts.

“There has been an unprecedented amount of government aid, which has made a difference for these lower-income families,” said Ana Hernandez Kent, senior researcher at the St. Louis Fed’s institute. “But when this aid ends, there’s a big question mark. What’s going to happen to them?”

Black Americans, as well as Hispanic Americans, risk getting left behind, she said.

That’s exactly what worries Nick Howell of Twinsburg, Ohio. Though he kept his position as a restaurant manager and his wife was only laid off for one day from her job at a plastics factory, it was the federal government relief efforts that helped them stabilize their finances during the pandemic.

The deferral on payments on their combined $75,000 in student loans and the stimulus checks allowed them to move out of Howell’s parents’ home into a rental apartment, as well as pay off some credit card debt.

Howell, 39, landed a better job as a general manager of a local restaurant chain last month, but the family is still living paycheck to paycheck. The rising price of gas and groceries is putting further strain on their wallet, as are the medical bills for their 7-year-old son, who broke his arm last summer trying to recreate the sledding down the stairs scene in “Home Alone.”

The couple was hoping the Biden administration and Congress would agree to pass student loan forgiveness, but that doesn’t seem likely. So now they are dreading the return of their monthly payments this fall.

“How are we going to handle that?” asked Howell, who has a master’s degree in higher education. “We’re still where we were — in debt, trying to work it off and hoping for no car breaking down or kid expenses or anything to put us further behind.”